How Is Automotive Sector Driving Polymer Market Growth?

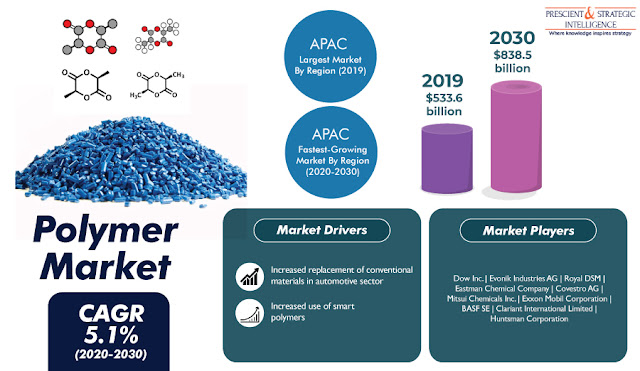

Due to a growing emphasis on a higher fuel economy, heavy materials, such as glass and metals, are being replaced by lighter variants, including polycarbonate (PC), in the automotive industry. As a result, the global polymer market size is expected to increase from $533.6 billion in 2019 to $838.5 billion by 2030, at a 5.1% CAGR between 2020 and 2030. This is because PC and other polymers have excellent electrical, mechanical, insulating, optical, and chemical properties, as well as a high strength-to-weight ratio and elasticity and corrosion resistance.

During the COVID-19 crisis, automotive plants across the world were shut down, in compliance with government mandates. This drastically reduced the demand for various raw materials, thus affecting the polymer market negatively. However, the demand for these materials in the food processing, packaging, pharmaceutical, and personal care sectors remained strong, as these industries are considered essential, therefore continued to operate during the pandemic.

Polymer Market Segmentation Analysis

The thermoplastics category, based on type, held the largest share in the polymer market in the past. The cost efficiency, high mechanical strength, and manufacturing ease of thermoplastics have made them vastly popular in the food packaging, construction, textile, automotive, and home appliance industries.

In the coming years, the polyethylene (PE) category, under the base material segment, will witness the highest value CAGR in the polymer market, of 5.6%. PE accounts for a high-volume consumption in the production of tubing products, packaging products, bottles, connectors, and plastic surgical implants, as a result of its high flexibility, stability, heat resistance, and impact resistance.

Major global polymer market players include Evonik Industries AG, Dow Inc., Eastman Chemical Company, Royal DSM, Mitsui Chemicals Inc., Covestro AG, BASF SE, Exxon Mobil Corporation, Huntsman Corporation, Clariant International Limited, Saudi Basic Industries Corporation (SABIC), and Sadara Chemical Company.

Source: www.psmarketresearch.com

Comments